2019 Archive

Sunday, November 10, 2019

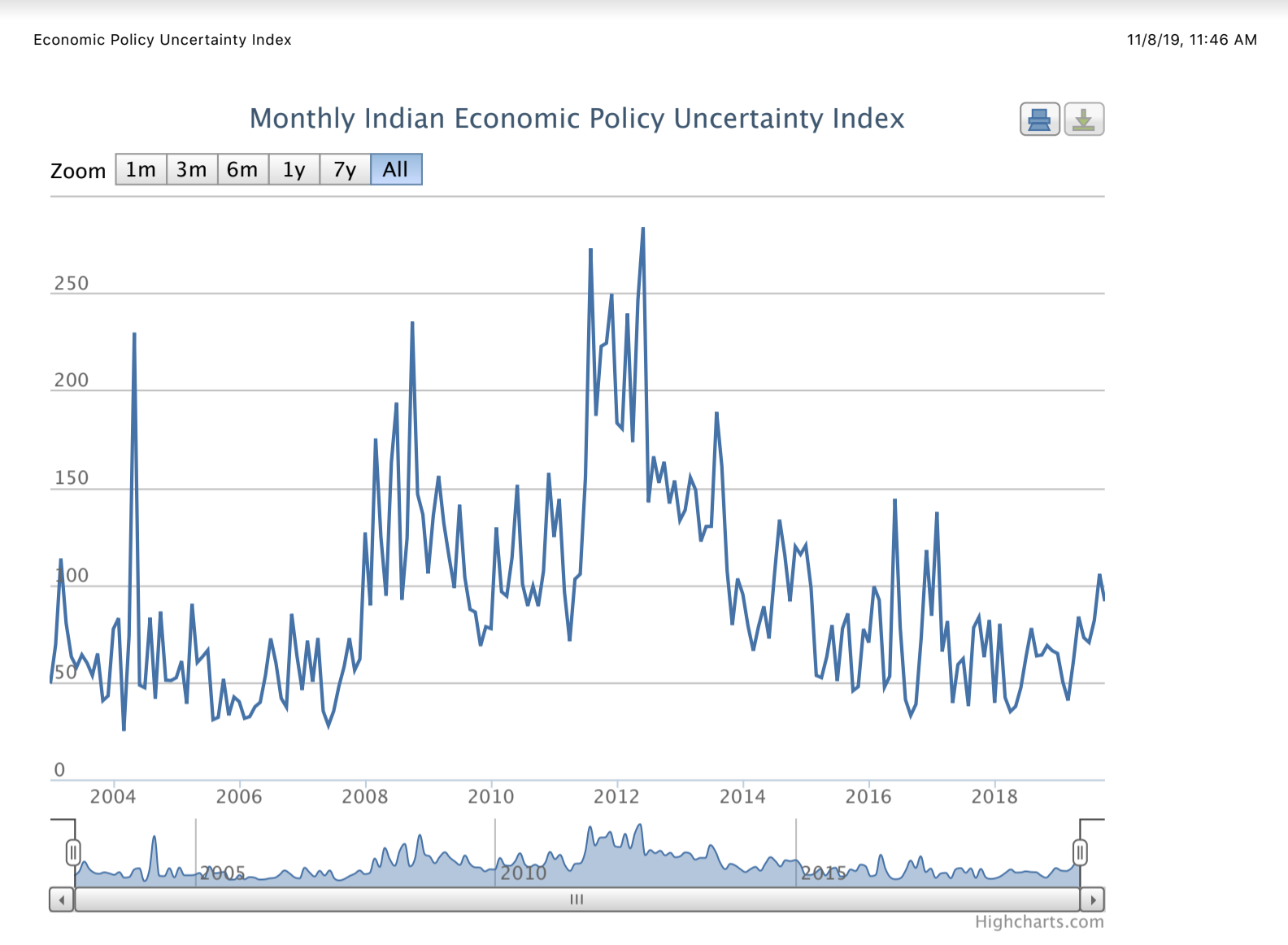

More on Uncertainty Creating Its Own Reality

The following two items from the daily CFA briefing [10/21] were interesting addendums to what was previously posted regarding how uncertainty can impact markets, cash flow and the economy.

Academic indexes show political events weighing on trading

Indexes developed by academics at Northwestern University, Stanford University and the University of Chicago show how political uncertainty worldwide is weighing down trading with a virtually unprecedented effect. Investors are responding by turning to cash and other defensive assets and are developing strategies to safeguard against a downturn. The Wall Street Journal (tiered subscription model) (10/2)

Loan growth slowed for top US banks

Loan growth for JPMorgan Chase decreased by $12 billion between July and September of this year while loan growth was slow for Bank of America, Citigroup and Wells Fargo. The decline in loan growth is not surprising because economic growth is slowing, according to Paul Ashworth, chief US economist at Capital Economics. CBS News (10/18)

Tracking Uncertainty

The attached article by May Wong details the creation of the World Uncertainty Index by Stanford economist Robert Bloom. More at: http://policyuncertainty.com/

Sunday, October 20, 2019

Uncertainty Creates Its Own Reality

William Rapp, Director, Leir Center For Financial Bubble Research

On a macro-economic level, we exist in a circular cash flow economy. When the economy is growing this leads to greater employment, which means there are more wages to be spent. Increased spending puts pressure on supply that leads to more investment and employment and thus more wages to be spent. It may also lead to increased borrowing and depending on the central bank higher interest rates to slow the economy and moderate inflationary pressures. Any fiscal stimulus can add to this circular cash-flow process by increasing employment directly or indirectly through increased purchases plus through tax cuts that increase after tax income.

But currently this circular flow of cash seems to be slowing despite lower interest rates and a big fiscal stimulus from massive tax cuts. Why? One obvious reason is the uncertainty surrounding the current environment due to the US trade and tariff wars with not just China but Japan, Canada, and the EU as well. When business executives or consumers face an uncertain economic environment, they naturally become less certain, less optimistic and more cautious. They then postpone major decisions until more information is available.

Check declining auto sales; reduced consumer confidence [Michigan Index]; fewer job offerings [“US employers advertised 7.1 million available jobs in August, down 1.7% from July's figure of 7.2 million, the Labor Department said. August was the third consecutive month of declining job openings”]; declining new hires per month, factories operating below capacity; low interest rates; low inflation; continued wage stagnation, slowing GDP growth domestically and globally.

However, it is not just the trade and tariff wars. As Engels explained in the 19th Century the Marginal Propensity to consume out of additional income declines with higher income and wealth. It may even approach zero for the super-rich. Thus, the large US tax cut that increased after tax income for the wealthy or corporations that then mostly used the funds for higher dividends or stock buybacks did little to stimulate the economy’s circular cash flow.

There was never any real capital constraint on businesses in terms of investment. Before the tax cut capital was readily available in abundance at ultra-low rates. Indeed, one might view the rise of the unicorns or the recovery of Greek credit as confirming this view. Since the fiscal stimulus was not spent continued slow growth and low inflation were then inevitable. Add the uncertainty of trade wars and slower growth in other countries and a more cautious economic environment has arrived.

This is not a static situation, though. The greater caution that results in fewer new hires and less investment means slower growth in the cash flow running through the economy. This leads to more caution and slower growth or even stagnation and then recession. This is how uncertainty can create its own negative reality just as confidence and optimism can create a more positive outcome. Those latter factors, though, currently seem in short supply.

[Repost from https://www.levyforecast.com/bubble-or-nothing/]

The U.S. business cycles that ended in the last three recessions involved progressively greater and more troubling risk-taking behavior. Each ended with worse financial fallout and a longer period of recession and weak recovery. Much has been written about the bubbles leading up to the commercial real estate deflation in the late 1980s and early 1990s, the crash of the tech stocks and the ensuing bear market of 2000-2002, and the deflation of home real estate and the debacle in mortgage-backed derivatives in 2006 through 2011. Yet analyses of the bubbles’ causes invariably omit a critical point.

The evolution of the economy’s aggregate financial structure has, over decades, altered the playing field for financial decision makers throughout the economy, increasingly skewing their available options toward higher risks, lower returns, or both.

This paper presents two facts that help explain economic and financial performance in recent decades and offers insights into the current business cycle, the 2020s, and beyond.

- Private sector balance sheets grew faster than income over many decades; thus, aggregate debt grew faster than aggregate income, and aggregate assets grew faster than aggregate income.

- This disproportionate balance sheet expansion changed financial parameters in the economy, mathematically making financial activity increasingly hazardous and compelling riskier behavior.

- From the mid-1980s on—the era of the Big Balance Sheet Economy—financial decision makers have had to choose between progressively lower returns and higher risk.

- Too much private sector debt relative to income has adverse consequences, of course, but so does an excessive total value of private sector assets relative to income. An extreme value of aggregate assets relative to income means meager yields and operating returns on assets, distorted financial decisions, and an economy vulnerable to asset price deflation.

- Each successive business cycle in the Big Balance Sheet Economy era has started with proportionately larger balance sheets and has involved more reckless balance sheet expansion leading to even bigger balance sheets and a worse financial crisis.

- Each successive crisis, with more bloated balance sheets to stabilize, was more difficult to resolve and therefore required the government to engineer dramatic new lows in interest rates, heavy fiscal stimulus, and other measures to stabilize economic conditions. The measures eventually overcame recession and chronic weakness, but in doing so they necessarily caused further expansion of balance sheets relative to income.

- During the 2000s, either the housing bubble or some other set of highly speculative, excessively risky, and destabilizing activities was virtually inevitable.

- Increasingly unsound risk taking has been occurring again in the 2010s.

- The present cycle is almost certain to end badly. Although there are signs that balance sheet ratios are undergoing an extended, secular topping process, they remain extreme and will produce serious financial instability during the next recession.

- There is no nice, neat solution to the Big Balance Sheet Economy dilemma, no blueprint for a politically acceptable resolution. The task of preserving prosperity while shrinking assets-to-income and debt-to-income ratios is, if not outright paradoxical, at least plagued by conflicting forces.

- Government policy cannot prevent serious consequences when the Big Balance Sheet Economy corrects, but it can moderate them and help households, businesses, and the financial system cope with them. However, these tasks would be difficult, politically tricky, and prone to cause some backtracking on balance sheet correction even if policymakers fully understood the economic problem.

- Although the outlook is fraught with uncertainties, individuals and organizations can benefit by taking steps to prepare for, endure, and in some cases capitalize on some of the developments ahead.

The U.S. economy continues to face a bubble-or-nothing outlook. Participants in the economy and markets will keep increasing their financial risk until the expansion breaks down, and the bigger the balance sheets are relative to income, the more severe the breakdown is likely to be.

Friday, September 20, 2019

Air Is Leaking From The Economy’s Tires

There are several signs based on prior experience indicating that not only are the US and Global Economies losing steam but the fuel that has propelled it, ultra-low interest rates, is not only losing its effectiveness but is becoming a threat to the financial system and the economy.

1) IPOs of money losing companies with “innovative” or “disruptive” business models are not doing well. Even if you can borrow at negative interest rates you still have to pay back the principal and a negative rate of 0.5% does not cover a 25-30% capital loss. Investors are thus becoming more risk adverse and are choosing value and low risk options as compared to growth and higher risk. This can become a self-fulfilling and self-reinforcing decrease in venture investment again affecting economic growth.

2) There is a huge BBB investment cliff in that this is where much of the ultra-low interest debt is located and if a firm’s credit rating falls below BBB or investment grade, then some institutional investors can no longer hold these bonds creating a double negative, because the firms affected will not be able to refinance easily leading to defaults. Since banks are now starting to issue CDS against some of these bonds this will magnify the effect of the defaults at the very time the FDIC is talking about reducing the capital that banks hold against such derivatives. This seems like a set up to repeat 2008 on some scale.

3) There has been a major disruption in global oil supplies due to the attack on Saudi Arabia’s oil fields and Iran is unlikely to have any reduction in sanctions, yet the oil price has not gone up anywhere near what one would expect indicating weakness in demand. This is another signal that the global economy is not growing robustly. This is confirmed by negative growth in the US, Chinese and Indian manufacturing sectors.

4) GM is sustaining a strike that neither side will win because there is over capacity in the auto sector and declining demand. Any vehicle GM makes can be bought from someone else and in the process GM will lose permanent market share plus replacement and service business. Even so the strike may persist, putting pressure on all the ancillary economies dependent on their continued operation leading to further business and consumer cutbacks. Real unemployment will rise even if it does not show up in statistics because the GM workers will not yet be looking for work.

5) Interest rate cuts while not assured will have less and less impact on the economy and markets due to the fact the economy is getting weaker and thus lower rates while being a small boost for equities, bond values and mortgage refinancing will not bring additional investment for the same reason that the large US tax cuts did not but instead mostly found their way into stock buybacks and increased dividends. If there is weak demand and excess capacity, then there is no need to borrow or use available cash for investment no matter how low the interest rates or increased after tax cash earnings. The problem is not cash availability but the need for new investment capacity that is the problem.

6) As the Fed and other Central Banks lower rates, they are pushing on a string while reducing their ability to deal with the existing slowdown or worse.

7) There are now 1.1 million less medically insured than last year. Therefore healthcare employment as a major job generator since 2008 has taken a hit.

8) Consumer confidence is now starting to emulate investor confidence. This could escalate quickly especially during the crucial holiday selling period. The China trade war does not help. This on again off again situation will only affect the markets not consumer or business behavior. Once uncertainty and volatility have been introduced, they are there until the downturn has gone its course. This is already being seen as businesses and consumers become more cautious and less optimistic.

9) All these factors can and are likely to interact so that a dramatic shift in any one of them can have a cascading effect. This means a Bear Stearns or Lehman or Anstalt Bank event or something else as yet unforeseen can act a trigger.

10) It will end badly because Central Banks have used up their tools propping up the current expansion. The Congress has also constrained the Fed’s ability to innovate. Given large government deficits fiscal policy may also be a less effective response

11) We are entering an unchartered road with a vehicle that may soon be running on its rims.

A Colin Clark Moment Once Again

In the 1930s Colin Clark a noted economist and statistician, completed a monumental study on world economic growth since the 19th Century. One important finding was that capital grows much faster than other factors of production and so periodically it burns itself up to bring production and consumption back into balance. We have seen this recently in the spectacular market declines of the nifty-fifties 1970s, Japan 1980s, Asia 1990s, Dot.com late 1990s, and the 2008-2008 housing, bond and stock market collapse.

Clark explains that these periodic capital burns, recently roughly every ten years, are because when a factor of production grows too fast, then the law of diminishing returns forces down earnings accruing to that factor. Where capital is concerned this leads to investors taking more risk to maintain income. Eventually this accumulated risk ends badly, and investors pull back seeking capital preservation over higher returns with way more risk.

We now seem to be in a Colin Clark moment, though not as spectacular as a stock or securitized debt market crash, though that may be coming. First is the appearance of negative interest rates in a wider number of markets. This effectively consumes capital even if very slowly. Secondly, several billion-dollar unicorns such as Uber have come to market at or below the prior financing valuations. Some such as WeWork have failed to come to market at all because the projected IPO values dropped far below some pre-market valuations. These earlier investors have thus lost a lot of money. Soon we may be hearing about unicorn investors what we heard about Texas oil barons early 1980s or dot.com billionaires around 2000. “How do you make a Texas/Dot.com millionaire? You start with Texas/Dot.com billionaire.”

Monday, June 3, 2019

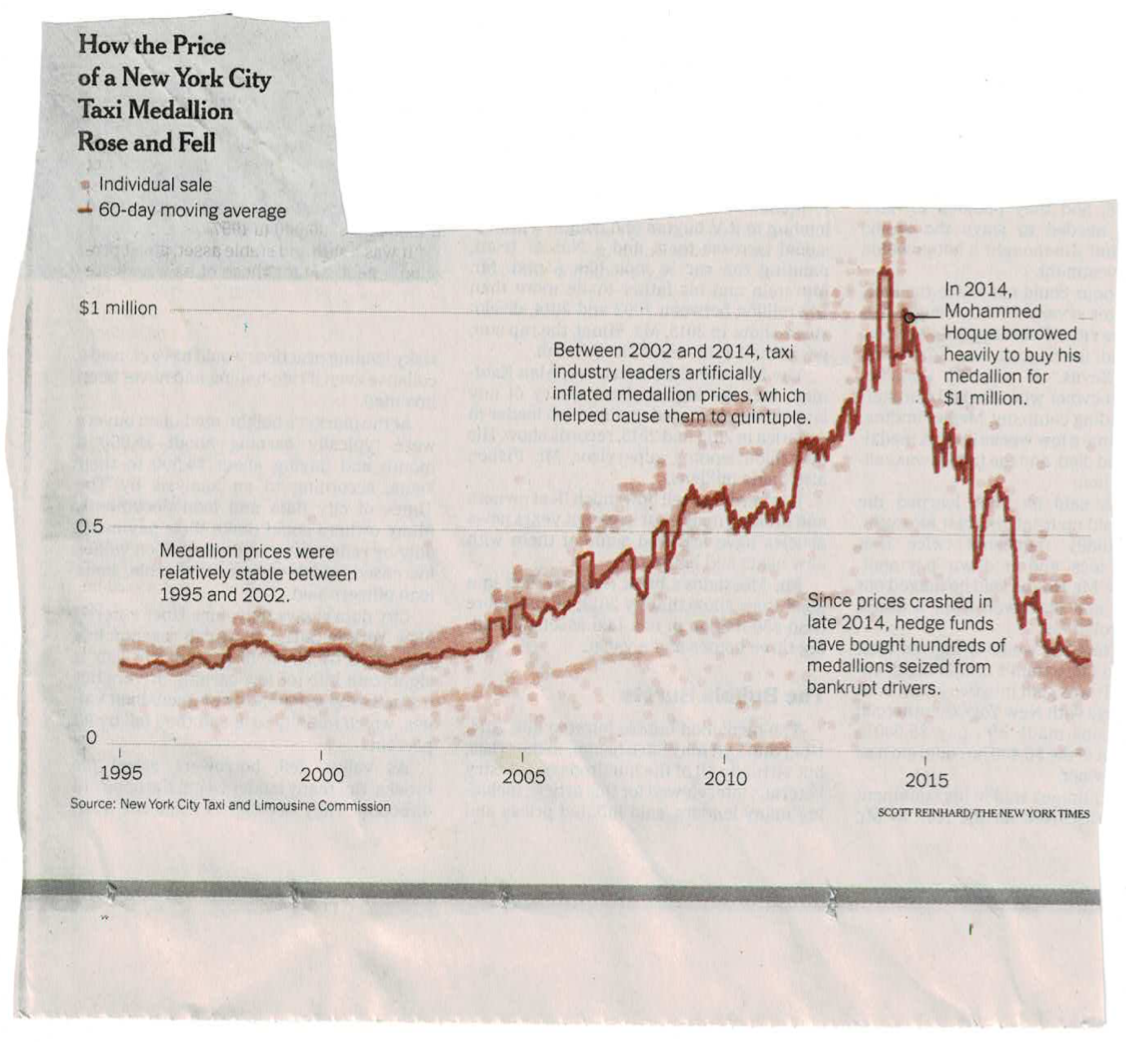

Visualizing The NYC Taxi Medallion Bubble

From the NYTimes's in-depth reporting on the Taxi Medallion Bubble in New York City.

Tuesday, January 1, 2019

Notes On The Chicago Fed’s Annual Forecasting Conference 2018

William V. Rapp, Martin Tuchman School of Management's Henry J. Leir Professor of International Trade and Business, and director of the Leir Center for Financial Bubble Research, attended and submitted his 2019 economic forecast at the Federal Reserve Bank of Chicago’s 32nd annual Economic Outlook Symposium held on November 30. His forecast is posted along with this brief summary of some of the highlights from the Conference which he also attended in 2017.

The Federal Reserve Bank of Chicago has provided the conference’s consensus outlook and later should provide slides from the various presentations on its website - https://www.chicagofed.org/events/2018/economic-outlook-symposium. The Fed’s median forecast results indicate that "the nation's economic growth rate is expected to be somewhat above its long-run average, the rate of inflation is predicted to tick down, and the unemployment rate is forecasted to be steady at a very low reading."

Additionally, real consumer spending is expected to "continue to grow at a moderate pace," while real business spending is predicted to "slow but remain solid." The expert consensus also points to growth in the housing market, a decrease in car and light-truck sales, and a slight drop in the price of oil. As for interest rates, the forecasters anticipate both the short-term and long-term interest rates to rise, by 56 and 35 basis points, respectively.

Professor Rapp was one of only two attendees noting a possible recession in 2019, a view that has subsequently gained more traction, though in his forecast he only predicted growth below the consensus.

However, unlike the consensus, his forecast does predict actual declines not only for autos but housing starts too due to a likely greater increase in Federal Reserve tightening than the consensus view. This is because he was the only forecaster at the conference that noted the large discrepancy between the CPI [Consumer Price Index] on which the Fed usually focuses and the GDP deflater which actually measures US inflation without the impact of lower prices due to imports and a strong dollar. Between 2012 and 2017 the GDP deflator on average rose 1.6% per year, roughly in sync with the CPI. But in the first nine months of 2018 it jumped to over 3.2%, a percent or more above the CPI and the Fed's target inflation rate.

Some other observations from the Conference were:

- Conferees were much less optimistic about the economic outlook for 2019 than a they had been about 2018 at the 2017 Conference. Any over-optimism had definitely faded.

- Fed could not readily explain the sharp difference between the CPI numbers and the GDP deflator, though they emphasized the Fed's policy focus is on the CPI.

- One possible explanation of the low CPI increase is the combination of the Engle's curve and the tax cut. As most of the tax cut went to the wealthy, who have low marginal propensities to consume, either directly or via corporations that used it to buy stock, the inflationary pressures on the CPI were weak while rising incomes fed into the GDP figures.

- China's huge excess steel capacity of as much as 500 million metric tons will be both a trade and political issue for some time and is directly related to China's slowing economic growth.

- China's slower growth is reflected in excess capacity in several industries in addition to steel as well as in its trade accounts and plant shutdowns. Mexico, Vietnam and Thailand are emerging as viable alternative supply chain sources.

- Further its Belt and Road initiative is now experiencing pushback from some recipient countries concerned about debt, economic sovereignty, and local jobs.

- Japan and Germany are increasing their shares of the global car market.

- Dollar will get stronger and precious metals weaker during 2019.

- Finally, it was noted that given any increase in major bankruptcies that it would pay issuers of Credit Default Swaps to buy the underlying debt at a discount, which would be good for bondholders.